The IRS collected over $4.9 trillion in taxes during fiscal year 2023, according to the IRS Data Book — and behind that number are millions of people who fell behind, got buried in notices, and reached out for help only to find that the help they got made things worse, not better.

Most conventional approaches to IRS tax problems fail not because the people using them are careless. They fail because the structure of those approaches was never designed for the specific mechanics of IRS enforcement.

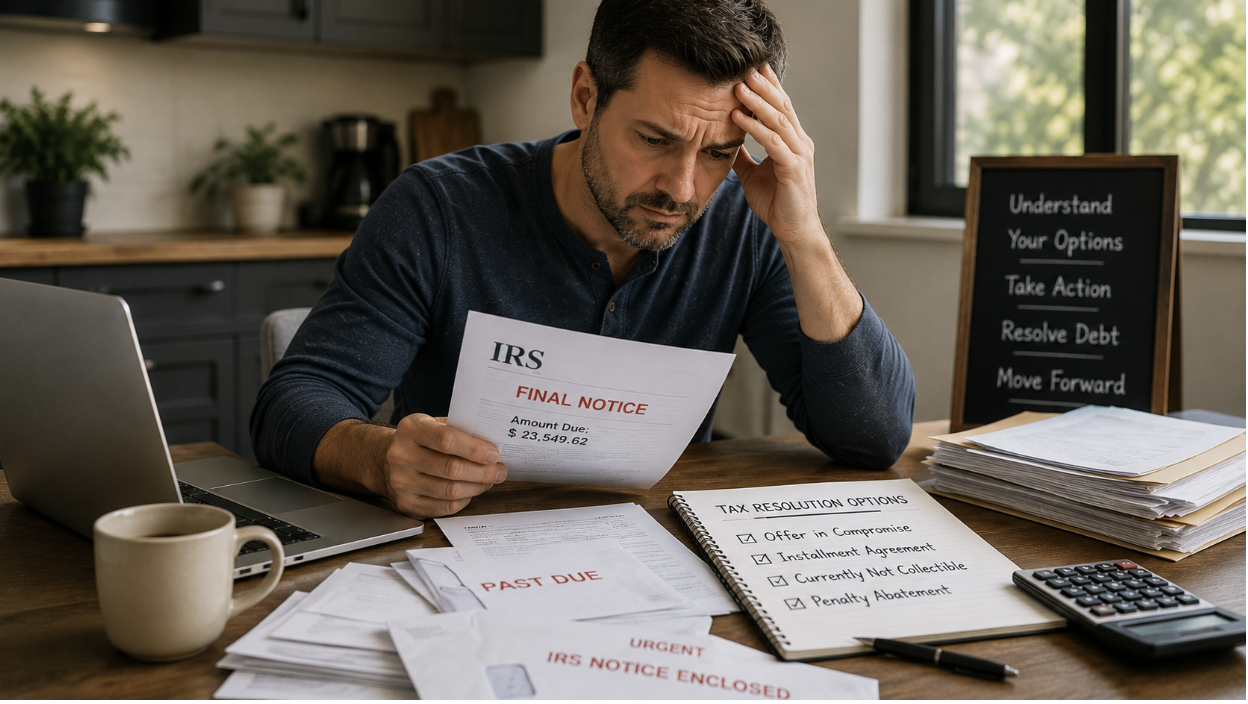

Key Takeaways

- The IRS resolution process has defined pathways — Offer in Compromise, Installment Agreements, Currently Not Collectible status — and the wrong pathway chosen early locks you into worse outcomes later.

- Wage garnishment can begin with as little as one missed response to an IRS Final Notice, making timeline management critical.

- Delinquent returns must typically be filed before any resolution program will be considered — resolution without compliance is not an option.

- DIY resolution and general tax preparers routinely misread IRS collection timelines, triggering enforcement that professional representation could have paused.

- A free consultation with a qualified CPA or enrolled agent is the fastest way to identify which resolution pathway actually applies to your situation.

What Actually Goes Wrong When People Try to Resolve IRS Tax Debt on Their Own?

Conventional IRS tax help fails because most approaches — DIY, general tax preparers, or high-volume resolution mills — treat IRS debt as a financial problem when it is actually a procedural problem. The IRS operates through a defined enforcement sequence with specific deadlines, response windows, and eligibility gates. Miss one gate, and the next option closes. The right resolution strategy depends entirely on where you are in that sequence, not just how much you owe.

The IRS does not get emotional about collections. It just keeps moving — and every missed deadline is a door that closes behind you.

Why Does the IRS Enforcement Process Feel Impossible to Navigate

The IRS enforcement sequence — the structured series of notices, deadlines, and escalating collection actions — is not intuitive. It was designed for compliance, not for clarity.

Most people receive a CP2000, CP503, or CP504 notice and respond the way they would respond to any bill: they either ignore it, call a general number, or attempt to negotiate directly. None of those responses engage the actual mechanism the IRS uses to determine next steps.

The IRS does not negotiate informally. Every resolution pathway — Installment Agreement, Offer in Compromise, Currently Not Collectible, Penalty Abatement — has a formal application process with specific eligibility criteria. Calling the IRS and explaining your situation does not pause enforcement. Filing the right form, through the right channel, at the right time does.

This is the structural reason conventional approaches break down. They address the surface problem (I owe money) without engaging the procedural reality (I have a narrowing window of options based on where I am in the enforcement sequence).

Aren’t All Tax Resolution Services Basically the Same?

No. And this is the most expensive misconception in the category.

High-volume tax resolution mills — the ones with national advertising and call centers — operate on a volume model. They take on large client loads, apply templated strategies, and move cases through a pipeline. The strategy that gets applied to your case is often the strategy that fits their workflow, not the one that fits your situation.

There is a meaningful difference between a firm that files an Offer in Compromise for every client because it is their primary product, and a CPA who evaluates your specific income, asset position, and compliance history to determine whether an OIC, an Installment Agreement, or Currently Not Collectible status actually serves you better. Understanding the warning signs of bad IRS tax help before you engage anyone is the fastest way to avoid compounding an already difficult situation.

The wrong resolution pathway does not just fail — it can reset your timeline and trigger enforcement you had temporarily avoided.

A business owner three years into penalty accrual on $80,000 in payroll tax debt came to Clear Tax Resolution after a national firm had filed an OIC that was rejected — because the client’s income made them ineligible. The rejection restarted the clock on IRS enforcement. The case was ultimately resolved through a structured Installment Agreement with penalty abatement, reducing the effective liability by roughly 30%. The total resolution took eleven months. The prior firm’s approach had cost the client eight months and additional penalties before the case was even properly assessed.

The Resolution Pathway Selection Problem: Why Getting It Wrong Early Costs the Most

The Resolution Pathway Selection Problem is the failure to match the correct IRS program to a taxpayer’s specific financial and compliance profile before any application is filed.

This is the root cause that most conventional approaches never address. It is not that people fail to try — it is that they try the wrong program, for the wrong reason, at the wrong stage of enforcement.

Here is how the major pathways actually differ:

| Resolution Pathway | Best For | Key Eligibility Factor | What It Does NOT Do |

| Offer in Compromise | Taxpayers who genuinely cannot pay full liability | Disposable income and asset equity below IRS threshold | Does not work if you have significant assets or steady income |

| Installment Agreement | Taxpayers who can pay over time | Ability to make consistent monthly payments | Does not reduce the underlying balance |

| Currently Not Collectible | Taxpayers in acute financial hardship | Income below IRS allowable expense thresholds | Temporary — IRS revisits annually |

| Penalty Abatement | Taxpayers with clean prior compliance history | First-time penalty or reasonable cause | Applies to penalties only, not principal or interest |

| Delinquent Return Filing | Taxpayers with unfiled returns | Must precede any resolution program | Does not resolve existing debt on its own |

> Choosing the wrong pathway is not a minor setback — it is the mechanism by which most IRS resolution attempts fail before they begin.

The IRS Reasonable Collection Potential (RCP) formula — the calculation the IRS uses to evaluate OIC eligibility — is precise and unforgiving. It accounts for monthly disposable income multiplied by a set number of months, plus net realizable equity in assets. Most taxpayers and general preparers underestimate what the IRS considers collectible, which is why OIC rejection rates remain high for self-prepared applications.

What Happens to Wage Garnishment If You Do Nothing?

Wage garnishment is not a threat. It is an automated outcome.

Once the IRS issues a Final Notice of Intent to Levy (CP90 or LT11), the taxpayer has 30 days to respond before enforcement begins. If no action is taken — no appeal filed, no resolution program initiated, no representative engaged — the IRS contacts the employer directly. The employer is legally required to comply.

The only mechanism that reliably stops an active wage garnishment is a formal levy release — and that requires either a resolution agreement already in place or a demonstrated hardship that qualifies the taxpayer for Currently Not Collectible status.

Calling the IRS to explain the situation does not release a levy. A properly filed Collection Due Process (CDP) appeal can pause enforcement, but it has a hard deadline tied to the notice date. Miss it, and the appeal right is lost.

This is where professional representation earns its cost. Clear Tax Resolution has handled cases where levy releases were secured within days of engagement — not because of any special relationship with the IRS, but because the right form was filed through the right channel before the enforcement window closed. What IRS tax resolution actually looks like in practice — including realistic timelines for levy releases and other enforcement responses — is something most people don’t learn until they’re already in the middle of it.

The One Thing Most People Get Wrong About Delinquent Returns

Filing delinquent returns makes your situation worse.

That is the conventional fear. It is also exactly backward.

Unfiled returns are the single largest barrier to IRS resolution. The IRS will not consider any resolution program — no OIC, no Installment Agreement, no hardship status — while returns remain unfiled. More critically, when returns are not filed, the IRS files Substitute for Return (SFR) assessments on the taxpayer’s behalf. SFR assessments use the least favorable filing status, claim no deductions, and often produce a tax liability significantly higher than what the taxpayer actually owes.

Filing delinquent returns almost always reduces the assessed liability. Not filing almost always increases it.

A self-employed contractor with five years of unfiled returns had an IRS-assessed balance of $142,000 based on SFR filings. After delinquent returns were properly prepared and filed with legitimate business deductions, the actual liability dropped to $61,000 — before any resolution program was applied.

Who Is This Approach NOT Right For?

Honest answer: professional IRS resolution is not the right fit for everyone.

If you owe less than $10,000 and have a clean filing history, the IRS Fresh Start program offers streamlined Installment Agreements you can set up directly through IRS.gov without professional help. The process is straightforward at that level.

If your tax issue is primarily a documentation dispute — a CP2000 notice about unreported income you can easily verify — a response letter with supporting documents may resolve it without representation.

Professional resolution services deliver the most value when the situation involves multiple years of delinquency, active enforcement (garnishment or levy), complex income situations, or prior failed resolution attempts. That is where the procedural knowledge and timeline management justify the cost. How Clear Tax Resolution actually works — the specific method used to assess, sequence, and execute resolution — explains why the approach differs from what most people have already tried.

Clear Tax Resolution is direct about this in consultations. The goal is the right outcome, not the largest engagement.

Frequently Asked Questions

How long does it actually take to resolve IRS back taxes?

It depends on the pathway and the complexity of the case. Installment Agreements can be established in weeks. An Offer in Compromise typically takes six to twelve months from submission to IRS decision, sometimes longer. Currently Not Collectible status can be established faster if the financial hardship documentation is complete. A qualified CPA can give you a realistic timeline after reviewing your specific situation — not a general estimate.

Will the IRS really accept less than I owe through an Offer in Compromise?

Sometimes, yes — but eligibility is based on a precise formula the IRS calls Reasonable Collection Potential. If your disposable income and asset equity exceed what you owe, the IRS will reject the offer. Most rejected OICs fail because the applicant did not qualify to begin with, not because the IRS is unreasonable. A professional assessment before filing is the only way to know if you’re actually eligible.

Can I stop a wage garnishment that has already started?

Yes. An active levy can be released through a formal agreement with the IRS — an Installment Agreement, an approved hardship status, or a pending CDP appeal. The process requires filing the right documentation quickly. The longer a garnishment runs without a formal response, the more difficult the release becomes. Professional representation significantly shortens this timeline.

What if I haven’t filed taxes in several years — is it too late?

It is almost never too late to file delinquent returns, and filing almost always improves your position. The IRS generally requires the last six years of returns to be filed before considering resolution options. The sooner delinquent returns are filed, the sooner the resolution process can begin. Waiting does not reduce the liability — it increases it through continued penalty accrual.

Do I have to come into an office to work with a tax resolution firm?

Not with Clear Tax Resolution. The firm handles cases entirely remotely — document collection, IRS communication, and resolution management are all handled without requiring in-person meetings. This is particularly useful for clients outside the New York area or those managing work and family obligations alongside an already stressful situation.

What is the difference between a CPA and an enrolled agent for IRS representation?

Both CPAs and enrolled agents are authorized to represent taxpayers before the IRS in all matters, including audits, collections, and appeals. A CPA brings broader financial and accounting expertise, which is particularly valuable when delinquent returns need to be prepared as part of the resolution process. An enrolled agent specializes specifically in tax matters. The key is that both credentials carry full IRS representation authority — unlike general tax preparers, who cannot represent clients in collections matters.

How do I know if I actually qualify for tax debt relief? Qualification depends on your income, assets, filing history, and the type of debt involved. There is no universal answer, which is exactly why a free consultation exists. Clear Tax Resolution’s initial consultation is designed to assess your specific situation and identify which pathways are realistically available — not to sell you a program. You will leave knowing more about your options than when you arrived, regardless of whether you move forward.

You Have Read This Far Because the Situation Is Real

If you are carrying IRS debt, facing garnishment, or sitting on years of unfiled returns — the stress is not just about the money. It is about not knowing what comes next, and whether anything you do will actually help.

The next step is not complicated. Call Clear Tax Resolution at 516-209-2594 for a free consultation with Guy A. Finocchiaro, CPA. Bring what you have. You do not need to have everything organized. The conversation will tell you exactly where you stand and what options are actually available to you — not what sounds best, but what fits your specific situation.

That is the only way to stop guessing and start moving.

References

IRS Data Book — Annual publication covering IRS enforcement activity, collection statistics, and taxpayer compliance data. Published by the Internal Revenue Service (IRS.gov).

IRS Collection Due Process (CDP) — IRS.gov guidance on taxpayer appeal rights following Final Notice of Intent to Levy.

IRS Offer in Compromise program — IRS.gov documentation covering eligibility criteria, Reasonable Collection Potential formula, and application process (Form 656).

IRS Substitute for Return (SFR) program — IRS.gov documentation on IRS-prepared returns for non-filers and the assessment process.

IRS Fresh Start Initiative — IRS.gov program overview covering streamlined Installment Agreement eligibility thresholds and expanded OIC criteria.