The IRS doesn’t care that you’re overwhelmed. It has a collection process, and that process runs on schedule whether you’ve found the right help yet or not. Choosing the wrong tax resolution service, or delaying while you figure out who to trust, doesn’t pause anything. It just costs you more time and, often, more money.

Evaluating tax resolution services is how you identify a qualified professional who can actually stop IRS enforcement, as opposed to one who takes your retainer and stalls. Look for verifiable credentials (CPA), a transparent process with defined steps, honest case assessments that include realistic outcomes, and clear communication about fees before any work begins. Avoid firms that lead with settlement guarantees.

Key Takeaways

- Credentials matter more than advertising: CPAs and have legal authority to represent you before the IRS; general “tax consultants” often don’t.

- A trustworthy firm explains your options before asking for payment. Not after.

- The most confident pitch is the least trustworthy signal. Firms that guarantee specific outcomes are violating IRS guidelines.

- Inaction while you search for the “right” provider is itself a decision. And it compounds penalties daily.

- The comparison that matters isn’t between firms. It’s between acting now with qualified help versus waiting and letting enforcement escalate.

Why Does Choosing the Wrong Tax Help Make Things Worse?

Most people searching for tax resolution services are already behind. The IRS has sent notices. Maybe a levy is pending. Maybe wages are already being garnished. In that situation, the instinct is to find someone fast. And that urgency is exactly what bad actors in this industry exploit.

The mechanism isn’t complicated: pressure creates shortcuts in judgment. You hear a confident pitch, you see a low upfront fee, and you sign. Six months later, nothing has been filed, the IRS has moved forward, and you’re out the retainer.

The tax resolution industry has a real credibility problem. The IRS itself has issued consumer alerts about “tax relief mills”. High-volume firms that make aggressive promises, charge large fees, and deliver little. Knowing how to screen out those firms before you hand over money is the actual skill this article is teaching.

What Credentials Actually Tell You. And What They Don’t

Credential verification is where most people start, and it’s a reasonable first step. But it’s not the whole picture.

CPAs, Enrolled Agents, and tax attorneys are the three categories of professionals with unlimited representation rights before the IRS. That means they can communicate with the IRS on your behalf, negotiate, and represent you in collections proceedings. A “tax consultant” or “tax specialist” with no recognized credential cannot do this. At least not without a licensed professional co-signing every action.

Verify credentials directly. The IRS maintains a public directory of credentialed tax professionals at irs.gov/taxpros. If a firm’s representative isn’t in that directory, that’s a hard stop.

Here’s what credentials don’t tell you: they don’t tell you whether that professional has specific experience with your type of problem. A CPA who primarily does small business bookkeeping is not the same as a CPA who has spent years working IRS offer in compromise cases and wage garnishment releases. Credential plus relevant experience is the standard. Not credential alone.

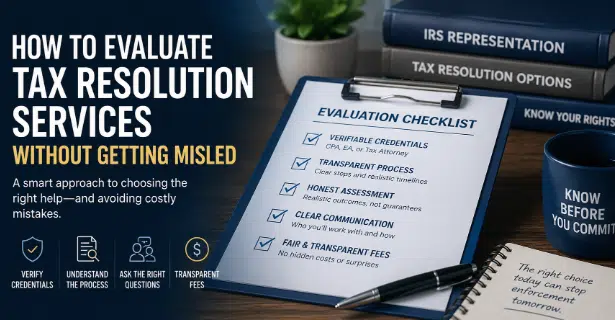

What Does a Trustworthy Evaluation Process Actually Look Like?

The Practitioner Evaluation Framework. A structured approach to screening tax resolution providers before committing, has five checkpoints. Use it in order.

Checkpoint 1: Initial consultation quality. A legitimate firm gives you a free consultation that results in an honest case assessment, not a sales pitch. Not a vague promise to “see what they can do.” A real assessment tells you which resolution options you likely qualify for, what the IRS’s current enforcement posture is on your account, and what realistic outcomes look like. If the consultation is mostly about their fees and success stories, that’s diagnostic.

Checkpoint 2: Fee structure transparency. Ask for an engagement letter before signing anything. Legitimate firms can tell you what they charge and why. Avoid any firm that asks for a large lump-sum retainer with no itemized breakdown of services, or one that ties fees to the size of your “settlement.”

Checkpoint 3: Guarantee language. Any firm that guarantees a specific settlement amount or promises to “eliminate” your tax debt is making a claim the IRS doesn’t allow practitioners to make. The IRS Offer in Compromise program, for example, has specific eligibility criteria. Not every taxpayer qualifies, and no practitioner can guarantee approval. Guarantee language is a disqualifier, not a selling point.

Checkpoint 4: Communication structure. Ask directly: who will be your point of contact? How often will you receive updates? Will you be passed to a junior associate after signing? Firms that can’t answer this clearly often have a bait-and-switch structure where a credentialed professional sells the case and an uncredentialed staffer works it.

Checkpoint 5: Timeline realism. IRS resolution takes time. IRS installment plans can be established relatively quickly; an Offer in Compromise typically takes six months to over a year to process. A firm that promises resolution in “30 days” on a complex case is either lying or doesn’t understand what they’re doing.

The Comparison That Actually Matters

Most people frame this as: “Which firm should I pick?” The more accurate frame is: “What happens if I wait, go it alone, or use the wrong provider?”

| Scenario | Enforcement Risk | Outcome Predictability | Cost Reality |

| Qualified CPA representation now | Enforcement typically paused during active resolution | High. Practitioner knows the process | Professional fee vs. compounding penalties and lost options |

| Waiting to decide | Enforcement continues; penalties and interest compound daily | None. IRS moves on its own timeline | Highest long-term cost |

| DIY negotiation | IRS is not your advocate; you’re negotiating against a trained collector | Low. Most taxpayers don’t know what they qualify for | Appears free; often costs more in missed options |

| Unqualified “tax relief” firm | May stall enforcement briefly; rarely resolves the underlying problem | Very low. And you’ve paid for nothing | Retainer lost; problem unchanged or worsened |

The IRS representative on the phone is not your advocate, they’re processing your account.

Who Is This Approach Right For. And When Does It Matter Most?

This framework applies most directly when enforcement is already active or imminent. If you’ve received a CP1058 notice, a wage garnishment has started, or a bank levy is pending, you don’t have the luxury of a long search process. The evaluation still matters, but speed and decisiveness matter too.

Consider a typical scenario: a self-employed contractor receives a series of IRS notices over 18 months, ignores them while trying to catch up on delinquent tax returns, and eventually gets a bank levy. By that point, the IRS has already assessed penalties and interest on top of the original balance. A qualified practitioner can often stop the garnishment quickly and then work the underlying resolution. But the compounding that happened during the delay is permanent.

Honest limitation: not every tax debt situation requires the same level of intervention. A small balance with no enforcement action and a clean filing history is a different problem than $80,000 in back taxes with an active levy, a qualified firm will tell you that. One that treats every case identically regardless of complexity isn’t giving you a real assessment.

The right professional doesn’t just know the resolution options. They know which ones you actually qualify for and which ones will waste your time.

What Should I Ask in the First Call?

Four questions that separate qualified practitioners from everyone else:

- “What IRS resolution programs do I likely qualify for based on what I’ve told you?”. A real answer requires them to listen first. A vague answer means they haven’t.

- “What happens to my account while we’re working on this?”. They should explain how enforcement is paused or managed during active representation.

- “What’s your fee structure, and can I see it in writing?”. Non-negotiable.

- “Who specifically will be working on my case?”. The answer tells you whether you’re getting the practitioner you’re talking to or a junior processor.

Fine & Clear Tax Solutions, led by Guy A. Finocchiaro, CPA, uses a structured three-step process that covers exactly these questions before any engagement begins. The firm has 17 years of experience handling IRS collections, garnishments, and resolution cases. And offers a free consultation specifically designed to give you an honest assessment, not a sales pitch. They work remotely, so your location isn’t a barrier.

The most dangerous moment in a tax debt situation isn’t when the IRS sends the first notice. It’s when you’ve been searching for help long enough that enforcement has quietly escalated while you were deciding.

FAQ

How do I know if a tax resolution company is legitimate?

Check that their practitioners hold verifiable credentials, CPA, Enrolled Agent, or tax attorney. Legitimate firms offer a real case assessment before asking for payment, provide written fee agreements, and don’t guarantee specific settlement amounts.

Can I negotiate with the IRS myself without hiring anyone?

You can, but the IRS collector you’re speaking with is trained to collect the full balance. They won’t volunteer that you might qualify for an Offer in Compromise or penalty abatement. DIY negotiation often results in payment agreements that are larger than necessary because the taxpayer didn’t know what options were available.

How long does tax resolution actually take?

It depends entirely on the resolution path. An installment agreement can often be established in weeks. An Offer in Compromise typically takes six months to over a year. Penalty abatement requests vary. Any firm quoting you a specific timeline before reviewing your case is guessing.

What happens to IRS enforcement while I’m working with a tax resolution firm?

A qualified representative can often get enforcement actions paused, called a “collection hold”, while your case is in active resolution. This isn’t automatic, and it requires your representative to communicate directly with the IRS. It’s one of the concrete reasons representation matters during active collections.

What should I do if I’ve already paid a tax resolution firm and nothing has happened?

Contact them in writing and ask for a status update and a copy of everything filed on your behalf. If you can’t get a straight answer, you can file a complaint with your state’s CPA licensing board or the IRS Office of Professional Responsibility. You may also be able to recover fees through a chargeback if payment was recent. Don’t wait. The IRS isn’t waiting either.

If you’ve read this far, you’re not just looking for information. You’re trying to figure out whether you can trust someone with a problem that’s already costing you sleep. That’s exactly the right question to be asking. And it deserves a real conversation, not a form submission.

Call Fine & Clear Tax Solutions at 516-209-2594 or schedule a free consultation to get an honest assessment of your options, your timeline, and what resolution actually looks like for your specific situation. No obligation. No sales pressure. Just the information you need to make a decision.

About the Author

Fine & Clear Tax Solutions is a CPA-led tax resolution firm with 17 years of experience helping individuals and business owners resolve IRS debt, stop enforcement actions, and file delinquent returns. Led by Guy A. Finocchiaro, CPA, the firm serves clients across the country through remote representation, offering personalized resolution strategies for taxpayers facing wage garnishments, back taxes, audits, and IRS collections.